Digital payments in 2026 are no longer defined only by cards, wallets, or QR codes. A major shift is underway toward account-to-account (A2A) transactions, commonly known as “Pay by Bank.” This model allows users to pay directly from their bank accounts without relying on traditional card networks or third-party intermediaries. As financial systems become faster, more connected, and more regulated around Open Banking frameworks, Pay by Bank Account is emerging as a core pillar of the global payments ecosystem. Solutions like https://www.fenige.com/products/pay-by-bank-account are part of this transformation, enabling businesses to accept direct bank payments with improved speed, security, and cost efficiency.

The Rise of Pay by Bank in the Open Banking Era

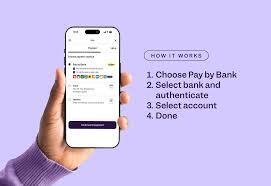

The foundation of Pay by Bank lies in Open Banking, which enables secure access to banking systems through APIs. This infrastructure allows payments to be initiated directly from a customer’s bank account, bypassing traditional card rails. In 2026, this approach is rapidly moving from niche adoption to mainstream usage across many markets.

Account-to-account payments are increasingly recognized for their efficiency. They eliminate unnecessary intermediaries, reduce transaction costs, and enable real-time settlement between banks. As a result, merchants receive funds faster while customers experience a smoother checkout process. This shift is part of a broader global movement toward faster payment infrastructures and embedded finance systems that prioritize direct bank connectivity over legacy systems.

Why Consumers Are Adopting Pay by Bank Faster Than Ever

Consumer behavior is a major driver of this transformation. People increasingly expect payments to be instant, frictionless, and secure. Pay by Bank meets these expectations by using strong bank-level authentication instead of manually entered card details.

One of the key advantages is trust. Since transactions are confirmed directly through a customer’s bank, users feel more secure compared to sharing card information across multiple platforms. Additionally, authentication methods such as biometric verification and secure banking apps reduce fraud risks significantly.

Convenience also plays a major role. With Pay by Bank, users no longer need to remember card numbers, expiration dates, or CVVs. A simple bank authorization is enough to complete a transaction in seconds, improving the overall user experience in digital commerce.

Business Benefits: Lower Costs and Faster Settlement

For businesses, Pay by Bank is not just a technological upgrade but a financial advantage. Traditional card payments often involve interchange fees, processing charges, and delays in settlement. In contrast, bank-to-bank payments significantly reduce these costs.

Real-time settlement is another critical benefit. Funds are transferred directly into merchant accounts without waiting periods, improving cash flow and liquidity management. This is especially valuable for e-commerce platforms, subscription services, and high-volume digital businesses.

Additionally, reduced dependency on card networks gives businesses more control over their payment infrastructure. It also minimizes payment failures caused by expired cards, insufficient limits, or network issues, resulting in higher conversion rates at checkout.

Security and Compliance in Modern Payment Systems

Security remains one of the strongest pillars of Pay by Bank adoption. Transactions are authenticated directly through regulated banking systems, which are typically subject to strict compliance standards and multi-factor authentication requirements.

In 2026, regulatory frameworks across different regions are also pushing for stronger identity verification and fraud prevention measures. This aligns well with Pay by Bank systems, which inherently reduce exposure to card fraud and data breaches by avoiding the storage of sensitive payment credentials.

As digital payments expand, compliance with Open Banking standards and secure API-based infrastructure ensures that Pay by Bank remains both scalable and trustworthy for global adoption.

How Pay by Bank is Reshaping E-Commerce and Digital Platforms

E-commerce platforms are among the biggest beneficiaries of Pay by Bank integration. Checkout experiences are becoming faster and more seamless, reducing cart abandonment rates and improving conversion rates.

Instead of lengthy card entry forms, users are redirected to their banking app or authentication screen to approve payments instantly. This streamlined process reduces friction significantly, especially on mobile devices where speed is critical.

Digital platforms are also embedding Pay by Bank into subscription models, marketplace transactions, and utility payments. This creates a unified payment ecosystem where users can transact directly from their bank accounts across multiple services without switching payment methods.

The Role of Fenige in the Pay by Bank Ecosystem

Companies like Fenige are playing a key role in expanding access to modern payment infrastructure. Their solution https://www.fenige.com/products/pay-by-bank-account enables businesses to integrate Pay by Bank functionality into their existing systems efficiently.

By offering direct bank payment capabilities, Fenige helps merchants reduce dependency on traditional card networks while improving transaction speed and reliability. This aligns with the broader industry shift toward Open Banking-driven financial ecosystems where payments are faster, more transparent, and more cost-efficient.

The Global Expansion of Account-to-Account Payments

Across Europe, Asia, and emerging markets, A2A payments are becoming increasingly mainstream. Governments and regulators are encouraging real-time payment systems, while banks are modernizing infrastructure to support instant transfers.

This global expansion is also supported by consumer familiarity. As users grow accustomed to digital-first financial experiences, Pay by Bank is becoming a natural extension of mobile banking and digital wallets.

Cross-border payments are another area of growth. While traditional international transactions often take days, A2A systems combined with modern settlement rails are reducing delays and improving transparency in global commerce.

Challenges and Future Outlook

Despite rapid adoption, Pay by Bank still faces challenges. Merchant awareness, inconsistent regional infrastructure, and user education remain key barriers. Some markets also lack fully mature Open Banking frameworks, which can slow down implementation.

However, the long-term outlook is strong. As more countries adopt instant payment systems and regulatory standards converge, Pay by Bank is expected to become a default payment method in many digital ecosystems.

Artificial intelligence, embedded finance, and digital identity systems will further enhance its capabilities, making transactions even more seamless and intelligent in the coming years.

Conclusion: A New Era of Digital Payments

Pay by Bank Account is fundamentally transforming how money moves in the digital economy. By enabling direct, secure, and instant bank-to-bank transactions, it reduces reliance on traditional payment intermediaries and enhances both consumer and merchant experiences.

With solutions like https://www.fenige.com/products/pay-by-bank-account supporting this shift, 2026 is shaping up to be a defining year for A2A payments and Open Banking innovation. As adoption continues to accelerate, Pay by Bank is not just an alternative payment method—it is becoming the foundation of the next generation of digital payments.